At Baum CPA we are routinely asked about the tax implications of starting a ROBS, and all too often we are asked if an S-Corporation would make more sense.

For those who are not yet familiar with the term, ROBS stands for Roll-Over as Business Startup, where an entrepreneur restructures their 401k retirement plan to use the pre-tax investment money to fund a business venture. This blog has previously offered quite a few articles on the topic:

- The ROBS Arrangement Retirement Strategy

- How a ROBS Arrangement Works

- The Advantages of ROBS [Part 1]

- The Advantages of ROBS [Part 2]

A Common but Alarming Mistake

It is common for CPAs to preemptively recommend an S-Corporation for a ROBS business structure, stating that it offers more tax savings opportunities than a traditional C-Corporation. However, the answer is more complicated than those accountants are taking into consideration. Very few accountants have expertise in ROBS, and many factors weigh more heavily than a simple desire for alleged tax savings.

In this article we will cover the general differences between entity types, and then discuss other considerations for determining the right entity structure.

A Brief Overview of the Structural Differences between C and S Corporations

Here is a brief comparison of the differences between the tax attributes of C and S Corporations:

Most entrepreneurs prefer to file as S-Corporations so that as taxpayers they can avoid the C-Corporation tax rate of 21%. They also opt to file the S-Corporation election for the employment tax savings derived from their pass-through profits not being subject to employment taxes. However, because an S-Corporation cannot have a tax-exempt entity as a shareholder (e.g., the ROBS 401k plan), a ROBS Arrangement company must file as a C-Corporation.

But tax savings strategies are just one side of the coin. Let’s consider some other metrics that make the decision between C and S Corporations more dynamic.

Tax Savings vs. Debt Service

Here we take a look at the differences between borrowing from the bank and raising capital via ROBS. Most entrepreneurs use a ROBS Arrangement because they want to start a business — and that business calls for a substantial sum of money as initial working capital. So, let’s compare the differences between being your own bank and borrowing from one!

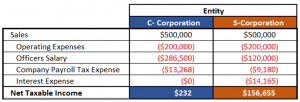

Say a business is expected to cost $400,000 for startup, and anticipates annually generating $500,000 from sales with $200,000 in operating expenses, before wages or interest expenses.

The entrepreneur is deciding between borrowing an SBA/bank loan of $400,000 –or– using $40,000 of personal funds and $360,000 from a retirement account in a ROBS Arrangement. The bank offers a 10-year loan at a 5% interest rate, subject to collateralizing the real property of the business. By using a bank loan, we can assume that the entrepreneur will elect to file as an S-Corporation and will have a salary as low as possible.

In a ROBS Arrangement, the owner would own 10% of the company (40,000 shares of 400,000 outstanding at $1 per share), and their 401k plan would own 90% (360,000 shares of 400,000 outstanding). The corporation would have no debt service payments on loans. Because a 401k plan owns 90% of this company, we can safely assume that this company is obliged to file as a C-Corporation. We will also assume that for tax purposes, the owner will pursue the highest reasonable salary to reduce Net Taxable Income to as close to zero as possible in order to avoid that 21% corporate tax rate.

Here’s what their respective income statements would look like:

In this example, the C-Corporation pays the highest possible salary to produce the lowest possible taxable income, thus opting to pay the lesser amount of company payroll tax instead of the higher corporate income tax. The opposite is true in the S-Corporation, as Net Taxable Income is only subject to personal income tax (which is not paid by the company), thus encouraging the shareholder(s) to receive a lower salary and report higher profits.

How do these decisions impact a married taxpayer from a tax perspective? Let’s assume that the state corporate tax rate and state personal income tax rate are both 4%. We also note that unemployment tax is the same regardless of entity choice, and is therefore not included in the following:

Considering that the total taxes quantified here are combined corporate and individual types of taxes paid, this illustration aims to show the total economic impact of taxation on the entrepreneur. Think of this bottom line as the total cashflow out of the taxpayer’s hands (in one form or another) and into government treasury coffers.

So, S-Corporations pay less tax — but what about the economic impact of debt service that affects the entrepreneur?

The Economic Impact of Debt Service that Affects the Entrepreneur

A $400,000 SBA/bank loan for the S-Corporation at 5% rate of interest, due to be repaid over 10 years can expect a monthly loan payment of $4,242.62. What is the impact in terms of dollars?

Suddenly the cost of debt has a BIG impact on the economic cost of each tax entity choice. Here is the grand total of the impact:

The cost of taxation and debt service difference is $39,072, favoring the ROBS C-Corporation (the S-Corporation costs nearly one-and-a-half times more, in this illustration).

Can you think of something better to do with an extra $39,000 lying around? I know I can!

Keep in mind that more or less debt the entrepreneur takes on will impact these results.

If you’re considering using a ROBS arrangement, you might want to call the experts at Baum CPA to discuss planning for your ROBS accounting needs. You can schedule an initial consultation with us by clicking here.

To learn more about ROBS tax implications and long-term benefits, please see ROBS C-Corporations vs. S-Corporations [Part 2]

This blog and its authors provide this content strictly for informational purposes. No content herein should be misconstrued as financial advice. Everyone’s specific circumstances vary — Always consult with a qualified, licensed financial advisor, legal counsel, and tax professional before venturing into any investment or business activities.